Introduction

The insurance industry is changing a lot, and AI is the main cause of it. Insurers cannot satisfy the customers anymore who have more and more expectations, they suffer from operational inefficiencies, and they are under pressure to save money. So, they have decided to use AI in order to be more competitive, agile, and creative.

AI is a very powerful tool that can be utilised for underwriting and risk assessment, fraud detection, and claims automated processing, to name just a few examples. Professed technologies such as Machine Learning (ML), Natural Language Processing (NLP), Computer Vision, and Generative AI are deployed in the main insurance processes to generate more intelligent decisions and greater customer satisfaction. According to a study conducted by McKinsey, AI may take over the insurance-related jobs done by half of the human workers by 2030, thus resulting in efficiency and customer happiness.

In addition to that, artificial intelligence is the reason why insurance companies can provide hyper-personalisation of their policies, intelligent customer communication, and proactive risk management. Few startups or traditional insurers are not readily putting in banks on the radically new AI that redefines the whole process of selling, servicing, and claiming the policies.

Here we will elaborate on the core of AI technologies that are drivers of the changes of the insurance sector, the practical use cases across auto, health, life, and property insurance, benefits, and the challenges of AI adoption, and the anticipated future trends. We will also discuss how platforms such as Emitrr assist insurance agents and companies in the process of changing and setting up the AI-powered automation and communication tools in line with the characteristics of today’s customer, who is mostly digital.

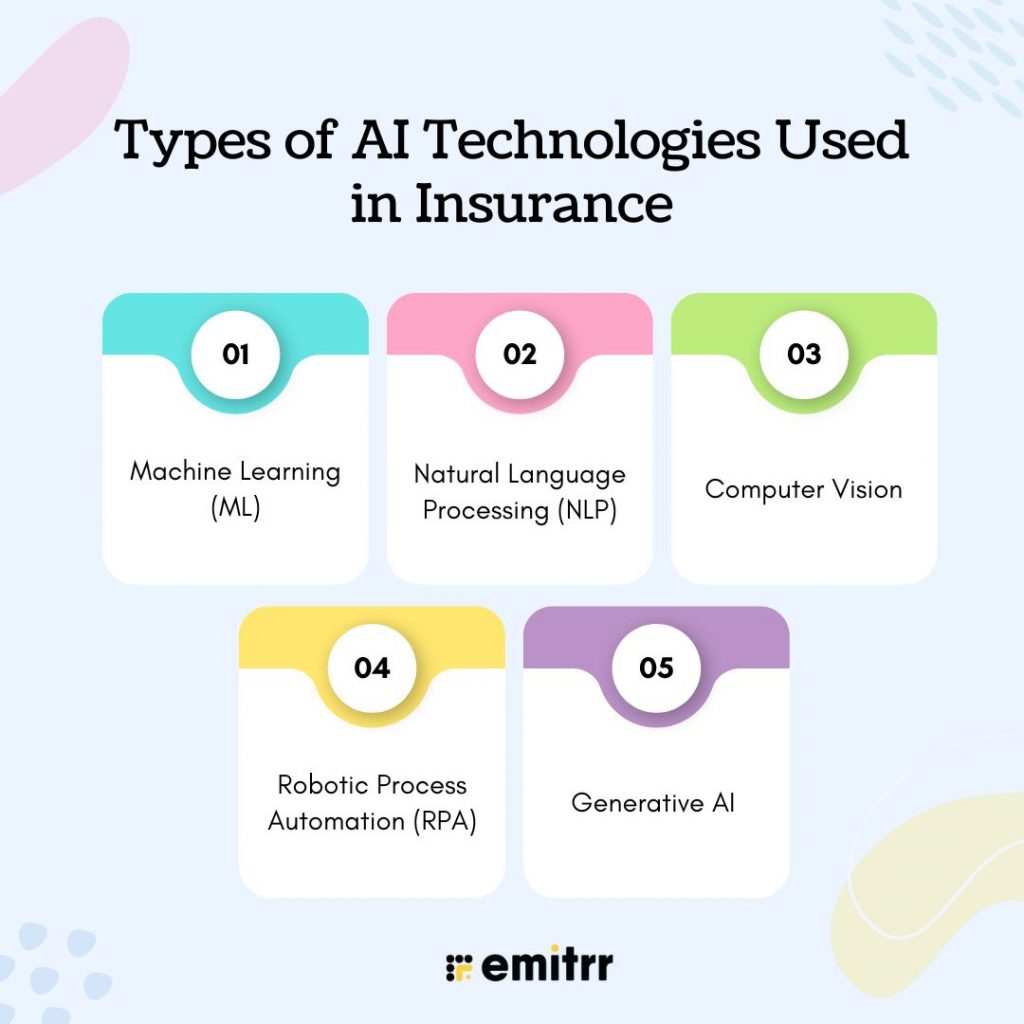

Types of AI Technologies Used in Insurance

AI in the insurance industry is supported by a variety of intelligent technologies that facilitate the creation, servicing, and management of policies in a new way. The operational efficiency, customer satisfaction, and risk assessment segments of the industry are being revolutionised by each AI subfield, with different subfields having various roles. The most significant AI technologies that are driving the insurance sector today are as follows:

Machine Learning (ML)

Machine Learning enables insurers to gain insight from vast amounts of structured and unstructured data for the identification of trends, the prediction of customer behaviour, and the undertaking of underwriting tasks without human intervention. Machine learning facilitates risk modelling, fraud detection, and dynamic pricing strategies by keeping track of previous claims’ data, customer interactions, and external risk indicators.

Example: For instance, ML algorithms can be utilised to decide how much the customer’s payment behaviour is influenced or to set the right premium price according to their behavioural data.

Natural Language Processing (NLP)

With the help of NLP, machines comprehend and respond to human language, which is the main factor for AI-driven customer service in insurance. Natural Language Processing (NLP) powers virtual assistants, claim triage bots, automated email management, and document summarisation. The major sources, such as policy documents, customer feedback, and support queries, are those from which insurers, with the help of NLP, extract key insights, so their manual processing time is significantly reduced.

Example: NLP can be used to make the AI chatbots that will solve the routine policy issues and the updates of the claims in real-time, 24/7.

Computer Vision

Computer Vision gives insurers the capability to go through visual data, such as photos or videos, in order to help them automate damage evaluation. It is prevalent in auto and property insurance to analyse images of car crashes or property damage, thus considerably facilitating the process of claims assessment, besides improving its accuracy.

Example: An AI model can identify a car dent’s severity via photos to go along with it; thus, it is no longer necessary to carry out inspections in person.

Robotic Process Automation (RPA)

RPA facilitates the execution of high-volume, rule-based tasks on the insurance lifecycle by employing such activities as data entry, policy renewals, compliance checks, and claims settlement processes. Thus, the operational speed is improved, and error is minimised, as well as human agents are given space to focus on highly valuable customer interaction.

Example: RPA bots can go through thousands of claims forms in a single day and automatically make payout transactions if these are done per the conditions.

Generative AI

Generative AI is the breakthrough that is assisting insurers in setting up policy recommendations that are individually tailored, in generating customer communications automatically, and even in product development by simulating customer scenarios. Generative AI gives a tool like Emitrr the power to carry out all the necessary tasks in a most personalised way, intelligent form replies, quick content creation, and staying consistent with regulatory tone and clarity.

Example: Emitrr’s AI assistant is capable of writing custom answers to customer emails, creating briefs of complex policy terms, and improving first-response time.

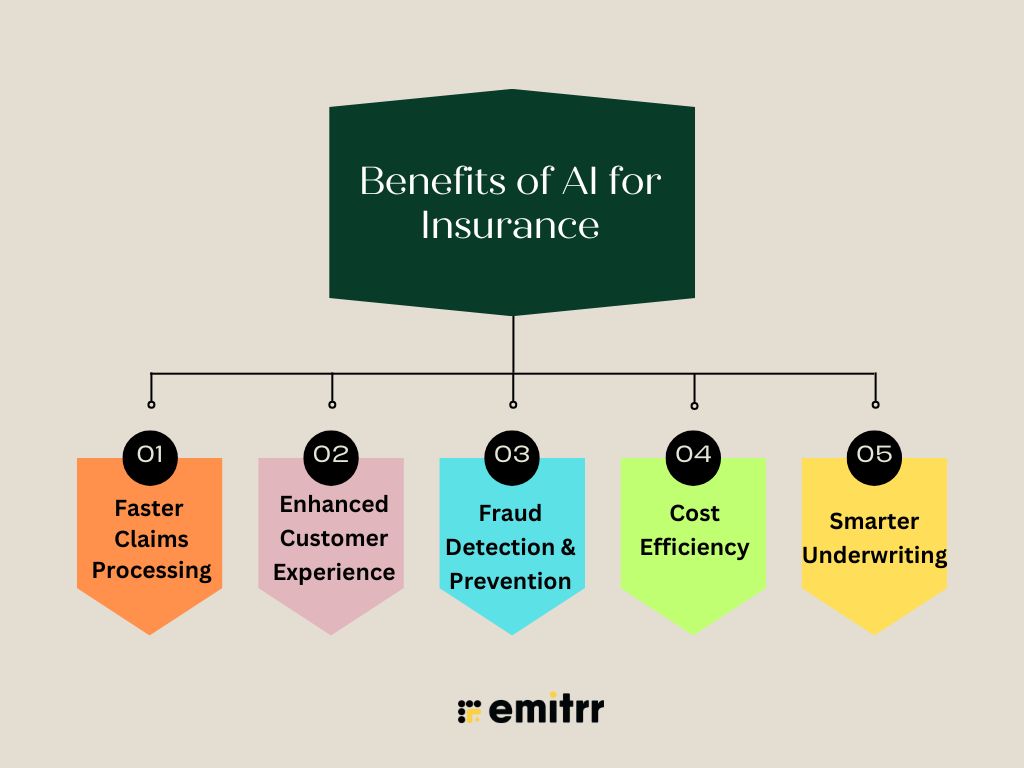

Benefits of AI for Insurance

Artificial Intelligence has become an absolute necessity in the insurance industry besides the competition factor only. Claim automation, fraud detection, and AI technologies are leading to improved efficiency, accuracy, and customization at every point of contact in the whole process. Here are the key benefits of AI adoption in insurance:

Faster Claims Processing

AI drastically reduces the time needed to submit, process, and conclude a claim. Insurers can use Robotic Process Automation (RPA) and Computer Vision tech to instantly analyze the images, verify the docs, and make the assessment of the situation, all of this is without human intervention. This allows for straight-through processing of simple cases, which can significantly shorten the settlement period from days to just minutes.

Example: AI systems can authorize low-risk car damage claims without human intervention if the damage photos are uploaded to the app.

Enhanced Customer Experience

Chatbots, and also virtual assistants powered by AI, have a 24/7 presence that can handle requests, update policies, and even walk customers through the claim process, all of this happening instantly. NLP and Generative AI facilitate the personalisation of interactions, ensuring policyholders receive the right information at the right time in a manner that feels like talking to a human.

Example: Emitrr is an AI-powered instrument that automatically generates email or text responses while maintaining context. This, in turn, helps increase response rates and retention.

Fraud Detection & Prevention

It has long been known that AI helps insurance product manufacturers detect deception and tricks by imposters. Such a range of tools is aimed at searching for the unnormal, suspicious and evil deeds, as well as some characteristic features which would hardly be recognisable to a human. For instance, machine learning algorithms will match the declared requests with previous fraudulent cases and can catch inconsistencies at once.

Example: AI systems are able to find duplicate claims or identify falsified accident pictures with Computer Vision technology.

Cost Efficiency

Insurance companies can save a significant amount of money with the help of AI which automates repetitive tasks, minimizes human errors, and provides self-service options. AI systems perform tasks such as policy servicing, renewals, and compliance documentation at a high volume, thereby decreasing the need for large support teams and call centers .

Example: AI-based automation enables underwriters to focus more on strategic evaluation and less on data gathering.

Smarter Underwriting

Artificial Intelligence facilitates an automated, data-oriented underwriting procedure that merges conventional actuarial data with unconventional sources- for example, telematics, social media activity, and the Internet Devices’ information. Risks are more effectively quantified by the machine learning models, hence personalized pricing and quick policy assignments are feasible.

Example: Lifesaving gadgets and health journals have become inextricably linked with life insurance underwriting, for online risk assessment in health care.

Use Cases of AI in Insurance

AI technology is radically reforming the insurance business. AI is here to change absolutely everything from customer support and underwriting to fraud prevention and policy personalization. Here are some of the most profound AI implementations in insurance at present:

1. AI Chatbots for Customer Service and FNOL

Through the customer lifecycle, AI-driven chatbots eliminate friction by maintaining continuous communication with policyholders. During the First Notice of Loss (FNOL), a chatbot can be particularly helpful. FNOL is therefore the first step in the claims process. Due to the natural language processing (NLP) technology, chatbots can entertain users’ queries, register them for the claim, and walk them through the process in real time.

Example: At 12 a.m. a dispatcher can give a claimant permission to use a chatbot as a guide that will lead them, with all steps and documents, till the end of the process.

- Emitrr’s Role: Emitrr’s AI assistant is utilized for carrying out inbound conversations. Channels like SMS, WhatsApp, and email can be used for this purpose. FNOL can be responded to by the AI component in the form of setting up a conversation, informing of the current status of the claim and auto-responding to questions asked by the policyholder frequently. In all these activities, it will keep using a tone human-like and voice and it will be available 24/7.

2. Claims Automation

Artificial Intelligence (AI) is a powerful ally in the claims life cycle as it can orchestrate data intake, verification decision-making, and even settlement. Machine Learning models (ML) give an impact assessment (through images or reports), confirm the policy, check for fraud, and, most importantly, they allow the payment to be carried out without the intervention of a human.

Example: For instance, in the field of automobile insurance, AI can capture and analyse images of the car damage, compare them with the policy, and settle simple claims within minutes.

- Emitrr’s Role: Emitrr is the integration of backend systems that can automate follow-ups, send out payment confirmation messages, and also take care of any status inquiries from claimants, thus both efficiency and customer satisfaction are optimized.

3. Fraud Detection

Defraud is a criminal activity that AI-systems use to carry out the detection of huge datasets with pinpoint accuracy. By the means of pattern recognition and anomaly detection, Machine Learning finds out abnormal claims behavior, repeated submissions, or counterfeited papers. AI highlights shady transactions early thus reducing instances of loss caused by fraud.

Example: The case can be when a system decides possibly the same person has filed a travel insurance claim twice but has used slightly different data to register.

4. Personalised Policy Pricing

Through AI insurers can personalize premiums by the help of data coming from the behavioral and situational context acquired in real time. This is how driving behavior (through telematics), health data (through wearables), or even geolocation may be used. This, in turn, brings about a more just, fair, flexible, and personalized pricing model, especially in the case of auto and health insurance.

Example: A cautious driver might be rewarded with lower auto insurance rates because their driving data, recorded by the in-car telematics device, has been consistent.

5. Customer Retention and Churn Prediction

AI tells the future of customers who are highly probable to leave by looking at their behavior, how they pay, the feedback they provide, and also the data from the interactions with customer support. Thus, insurers can initiate the call to be the first to send retention offers, policy changes, or personal communication.

Example: A customer who has not opened the company’s emails or missed reminders to renew their subscription could be flagged by an AI-based scoring model as one that should be targeted in a win-back campaign.

Challenges & Disadvantages of AI in Insurance

Although AI is transforming the insurance business, it is also introducing a lot of difficulties in the implementation stage. The issues raised by data security and ethical considerations stand at the top of the list of problems that insurers face. They have to still use this technology in a responsible and effective way while keeping abreast of all these obstacles.

Data privacy and regulatory compliance (GDPR, HIPAA)

Insurance AI models heavily depend on sensitive information, such as health records, financial transactions, and behavioural data. The use of such data in a responsible manner implies that there must be a strict observance of global and regional privacy regulations such as GDPR, HIPAA, and CCPA.

The trust of the customer shall be maintained through building bulletproof AI pipelines and committing to the principle of utilising data transparently.

Potential bias in pricing models

If there are biases in the training data, the results in several areas, such as underwriting, pricing, and fraud detection, may be unfair or inconsistent. Besides, the use of the historical dataset, for example, may result in the perpetuation of the imbalances in demographics or socioeconomic conditions.

One of the key issues in this regard is the concept of continuous auditing, together with a testing of the bias and consequently updating of training data.

Integration with outdated legacy systems

Most insurers have legacy infrastructure that is not very flexible and does not have the capability to support AI applications of the modern era. The integration of AI with systems that manage the policy, claims, and customer service may be complicated and require a lot of resources.

Recovering interoperability is often very costly due to the substantial expenses associated with IT modernisation and change management.

Explainability of AI decisions (black-box problem)

One particular type of AI, deep learning machines, is often called “black boxes” as the decisions they make are not explainable. This, however, becomes a problem when insurers decide to reject the claim, change the premium, or indicate fraud, and then, they have to explain these decisions to customers or regulators.

The need for Explainable AI (XAI) frameworks that give transparency and also permit human supervision of the automated choices is on the increase now.

Ethical considerations in automated decision-making

The use of automated technology to make decisions in the fields of health coverage, life insurance eligibility, or claim payouts cannot help but lead to the arising of some ethical questions. Such processes may lack the presence of human context, which is needed to decide the fair treatment of unique or sensitive situations.

Traditional vs AI-Based Insurance Models

| Aspect | Traditional Model | AI-Based Model |

| Claims | Manual submission, document-heavy, longer turnaround times. | Automated FNOL (First Notice of Loss), faster triage, quicker settlements via AI-based workflows. |

| Customer Service | Limited to business hours, relies on human agents, slower query resolution. | 24/7 AI-powered chatbots and voice assistants, instant query handling, and multilingual support. |

| Underwriting | Rule-based, depends on historical risk models and human judgment. | Data-driven risk assessment using predictive analytics and real-time behaviour data. |

| Policy Customization | Standardised plans with limited flexibility. | Hyper-personalised policies tailored through machine learning and customer data analysis. |

| Fraud Detection | Post-incident investigation, rule-based flagging. | Real-time fraud detection using anomaly detection and behavioural analysis via AI. |

| Operational Costs | Higher costs due to manual processes and human dependency. | Reduced costs through automation, faster processing, and optimised resource allocation. |

Where AI Outperforms Humans and Where It Doesn’t

Artificial Intelligence is redefining the insurance world, bringing a big impact, but it is not the case that human involvement is not necessary. It rather improves human capabilities by using it in the areas where AI is better for, while people retain their role of providing empathetic, high-context interactions, which are necessary.

Where AI Wins:

- Speed and scale of data analysis

AI can carry out the analysis of vast amounts of policy, customer, and claims data instantaneously, thus completing in the blink of an eye the work that would take human teams a long time, hence more informed decisions.

- 24/7 availability

Due to the use of AI chatbots and virtual assistants, it is possible to get support for any issue at any time of the day or night. This is because they are always available and can help with filing claims, getting quotes, or resolving FAQs.

- Accuracy in repetitive tasks

Processes such as claims triage, policy generation, and fraud detection that are high-volume and rule-based human error are reduced by AI.

Where Humans Excel:

- Empathy and ethical judgment

Human agents can introduce emotional intelligence into conversations with sensitive topics, for example, in the case where a claim is denied or discussions about life insurance. They ensure that trust and care are prioritised.

- Handling disputes and edge cases

Human reasoning, negotiation, and interpretations of the context for making decisions are often necessary in the case of complicated claims and exceptions. These go beyond the understanding of AI.

- Explaining complex decisions to customers

While humans are able to present technical information clearly and unfold terms of regulations and personal advice, AI, at present, is far from being able to do so as humans.

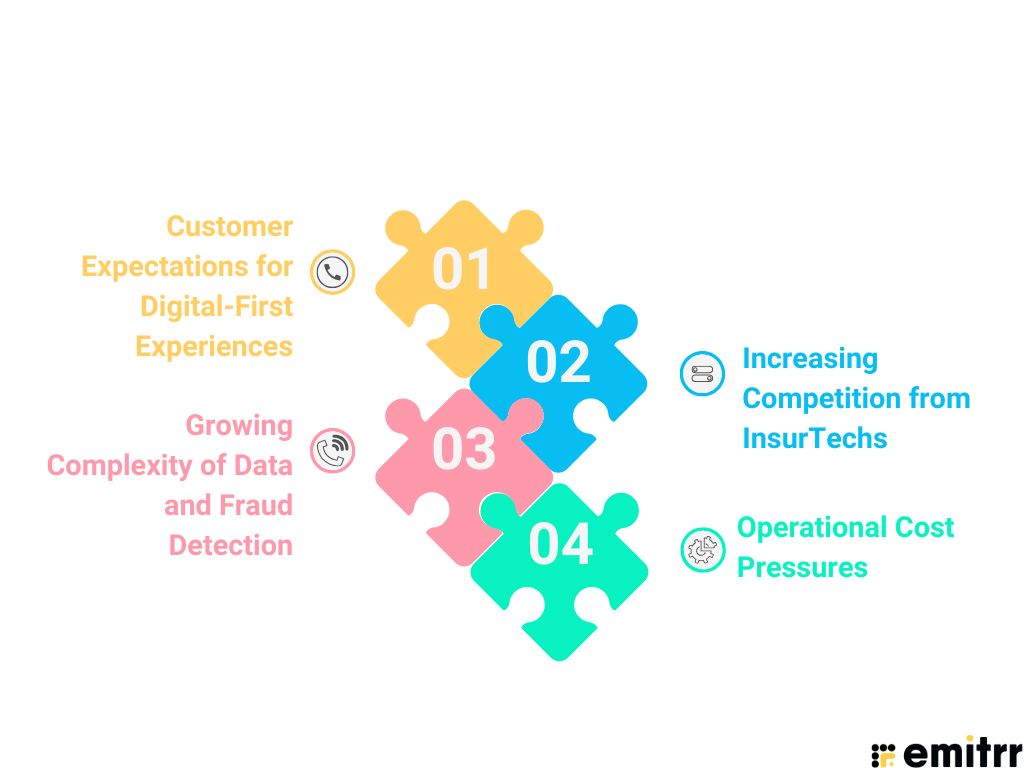

Why Insurance Businesses Need AI Now

Insurance business uses of AI have stretched beyond a speculative venture to become a critical prop for their competitiveness on the market. In the face of changes in consumer behaviour and worsening operational challenges, insurance companies have no option but to be very agile in order to remain relevant and profitable.

Customer Expectations for Digital-First Experiences

Currently, the insured individuals have the expectation that they will have immediate interaction, effortless registrations, and take care of the claims on their own without any human assistance, all this, however, must be conducted by AI-based systems. The use of chatbots, virtual agents, and AI-based policy recommendation engines augments convenience and satisfaction.

Increasing Competition from InsurTechs

Insurance startups that are digital-native are making use of AI to shake up the market through highly personalized products, along with instant approvals and predictive risk assessments. Traditional insurance companies need to incorporate AI, if they want to be at par with the new entrants, they have to be fast, flexible, and give personalized services.

Growing Complexity of Data and Fraud Detection

The quantity of formal and informal data (claims, IoT, social media, medical records) is growing rapidly. AI gives the insurers a chance to be ahead of the fraudsters by helping them to catch fakes at the earliest stage of the process, pointing out the anomalies, and risk modeling with much better accuracy in comparison with the traditional methods.

Operational Cost Pressures

Due to increasing administrative costs, insurers are now automating their manual tasks. AI facilitates a reduction in overhead expenses as it takes care of scheduling, information gathering, document verification, conversation, and even claim triage. This enables the organizations to be more efficient and also reduces their expenses.

Why Emitrr is the Ideal AI Communication Platform for Insurance

Insurance providers in today’s world require more than just automation, they also require intelligent, integrated, and emotionally aware communication. Emitrr, an AI platform built for purpose, is designed to eliminate communication bottlenecks in customer service, claims, and policy management. It is a special platform that facilitates communication across various departments in an enterprise.

AI Assistant

Emitrr’s smart virtual assistant carries out the tasks of engaging in routine conversations with policyholders, underwriters, and agents. Emitrr accomplishes these tasks by work reminders, providing answers to claim-status queries, and more, while reducing human workload.

Multilingual Chatbots

Emitrr’s multilingual chatbots ensure that people are at the center of the insurance industry. They also guarantee that the conversation is clear and will have the correct context in different languages, such as English, Spanish, Hindi, etc., thus eliminating language as a barrier and increasing the participation of diverse audiences.

CRM & Claims Integration

Emitrr perfectly matches the platform of your CRM and your software for managing the claims and your customer databases. This is done by uniting all your communication under one AI-powered hub with Emitrr. This, in turn, reduces the number of silos and ensures that there will be faster resolutions at every step of the journey of insurance.

AI Writing Tools

An AI writing assistant is the aid that helps the insurance teams of your company to speed up the process of generating clear and more empathetic messages. In case it is a new policy, or the denial note to

Emitrr’s AI text improvement suite has a great impact on insurance teams, enabling them to write better, faster, and with more empathy below the platform.

Help Me Write: Completes responses on the go from prompts, supplies examples of claim acknowledgements, policy updates etc.

Enhance –

- Make it Crisp: Eliminate the words that do not add any information to the message and make it more clear and concise.

- Make it Empathetic: It provides a professional and human tone for difficult aspects of the conversation such as claim rejection or delay.

Suggest a Reply: Gives a choice of responses for the message that arrives (for example, customer inquiries, status updates).

Note: Emitrr’s Professional Plans comprise these functionalities only.

24/7 Support

By giving the AI and humans the ability to collaborate 24 hours a day, 7 days a week, Emitrr guarantees that policyholders and stakeholders have.

Future Trends: What’s Next for AI in Insurance

Artificial intelligence is going to impact the insurance industry even more by its rapid development. It is forecasted that AI will influence strategic planning, improve claims transparency, optimize risk modeling, and revolutionize customer experience. These are the most significant AI-driven technological innovations that will set the course of the insurance industry in the future:

Explainable AI (XAI) for transparency and trust

With AI taking over a larger share of essential functions such as underwriting, claims processing, and pricing, the need for clear and fair decisions has become a hot issue. Explainable AI (XAI) is a technology that works on this principle by providing the models with an opportunity to present their train of thought in a language understandable by humans. This ability really is at the forefront of transparency and accountability in the insurance process, thus it helps to improve customer and regulator trust.

AI + Blockchain for secure claims processing

At the same time, AI and blockchain come together in the area of claims verification, they are not only good at that, but they are also changing the game completely. Blockchain is a technology that tracks it all and is tamper-proof; thus blockchain ensures the trust of the data it carries to be beyond any question and its verifiability. AI, on the other hand, takes over the task of claim verification; thus, it will both increase fraud detection and make the process of disbursing decisions more unambiguous, which in turn means that the claims process will be faster, fairer, and much more secure.

Wearables and IoT data in real-time underwriting

The insurers in their activities are very often turning to the data obtained from the users of wearable devices (such as fitness trackers) and IoT-enabled smart homes and vehicles. AI algorithms are intended to solve this problem of the continuous flow of behavioral data that they provide, thus the monitoring allows dynamic risk assessment and designing of hyper-personalized policies. This trend is a major game-changer for the health, auto, and home insurance sectors as it allows personalized premiums based on actual behavior.

Synthetic data to train fairer models

Insurance companies are addressing these biases in data from the real world by also using synthetic data. KPMG illustrates that insurers are now employing computer-generated data in order to develop their AI models. The strategy not only provides more variety in the sample sets, but also it becomes a lifeline in cases where the real-world data is lacking, incomplete or intrinsically biased. The upshot is the creation of more reliable and fair AI models.

AI-driven strategic planning

The revolution of AI in the insurance industry is changing the game from merely improving efficiency to making strategic decisions. Skilled AI systems enable insurers not only to manage their product portfolios efficiently but to also get a precise picture of market trends as well as customer turnover ahead of time. This, in turn, facilitates making strategic decisions faster, supported by data, which in turn fosters competitive advantage.

FAQs

Artificial intelligence is utilised throughout the entire insurance value chain, which includes underwriting, claims processing, fraud detection, and customer service. Tools such as machine learning estimate risk more precisely, whereas chatbots and voice AI facilitate customer support. Predictive analytics also allows insurers to come up with personalised policies and pricing.

Many AI platforms like Emitrr do offer subscription-based and scalable pricing that is suitable for small to mid-sized insurers. Moreover, the use of the cloud is becoming more and more widespread, which in turn decreases the need for infrastructure, and hence, the cost of AI adoption becomes more manageable than ever.

The answer is a definite no. AI is primarily designed to enhance human work rather than replace it. AI automates data entry and claims triage, freeing up time. This allows human agents to focus on nurturing customer relationships and providing strategic advice, where their skills are invaluable.

AI apparatuses that are involved in insurance are mandated to follow data privacy laws such as GDPR and HIPAA very strictly. Trusted companies install encryption from end to end, also nameless, and they access only the places with rigorous control to ensure the secrecy of the information.

Practice indicates that the expected return on investment (ROI) may come from the expenses that are avoided, the efficiency of work, lesser fraud, and the retention of customers. Research affirms that AI can accomplish 70% of shortening the handling time of the claim as well as increasing the conversion rate of the lead by above 30%.

Conclusion

Artificial intelligence is not just a concept from sci-fi anymore in the insurance sector, it is now the standard. The use of AI in speeding up claims processing and providing hyper-personalized customer experiences allows insurers to be more efficient, accurate, and in an empathetic manner.

Emitrr leads the charge in making this change happen. It provides insurance companies with a global AI chatbot, a customer service automation tool, CRM, and claims system integration as well as advanced AI writing skills, thus enabling teams to update communication, automate workflows, and increase operations without worrying.

Do not hesitate to embark on your Emitrr journey today and divert your attention from operational tasks to what is really important: establishing trust, keeping the customers, and pursuing sustainable growth.

Insurance’s future is all about being digital, smart, and AI-driven. Just be the one who is in charge of it.

4.9 (400+

reviews)

4.9 (400+

reviews)